Vanguard: Addressing the Retirement Crisis in America

As part of my Design Strategies class at NYU, we delved into a comprehensive project undertaken as Vanguard to address the retirement crisis in America. The project aimed to introduce innovative solutions to encourage more Americans and their families to save for the future and combat the challenges posed by insufficient retirement savings.

Project Horatio: How might we help more Americans and their families save for the future and combat the retirement crisis?

Table of Contents

1

Introduction

Retirement in the US

What is the Retirement Crisis in America?

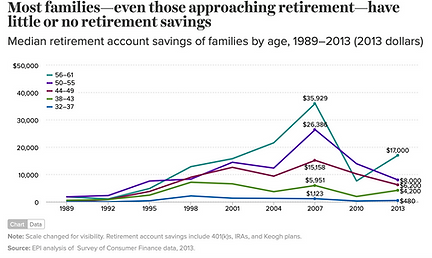

The U.S. retirement crisis has been building for decades, with an aging Baby Boomer generation straining social security and pension funds.

Between 2021 and 2040, U.S. states will grapple with a projected $334.3 billion increase in expenditures due to insufficient retirement savings.

Retirement Statistics

Over half of Americans (51%) fear running out of money in retirement

70% regret not starting to save sooner.

According to the National Retirement Risk Index, half of U.S. households will not be able to maintain their standard of living when they retire even if they were to work until age 65 and annuitize all their financial assets.

2

Problem Statement

How might we help more Americans and their families save for the future and combat the retirement crisis?

“

Strategy is about winning… it's about unique positioning, creating sustainable advantage and delivering superior value versus the competition.

AG Lafley

3

Opportunity Hypothesis

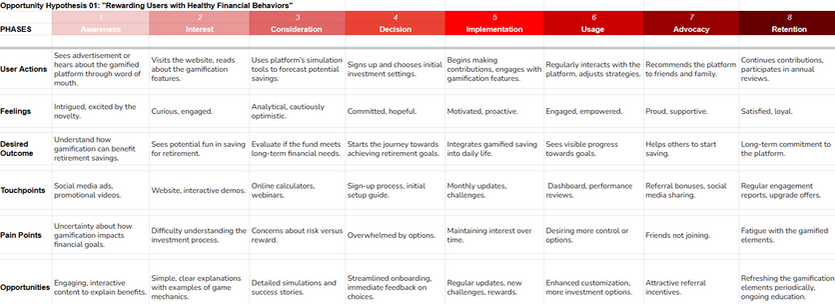

Opportunity Hypothesis 01

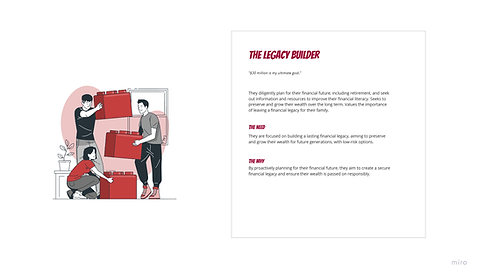

We believe there is an opportunity to introduce a novel Investment Fund model where contributions will be made for the child from birth (Where To Play Hypothesis) at every milestone such as a birthday, in order to drive long-term financial security (Target Outcome), in pursuit of providing a seamless and consistent savings mechanism from birth to retirement, thereby addressing the need for retirement planning early in life.

Opportunity Hypothesis 02

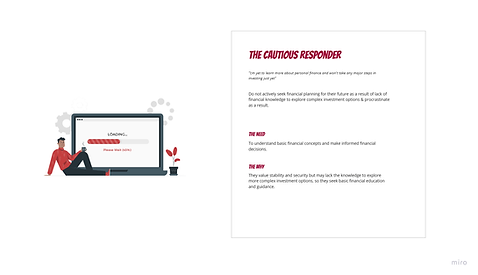

We believe there is an opportunity to utilize a behaviorally-driven platform with personalized challenges and rewards tied to saving for retirement (The Idea) in order to increase user engagement and incentivize them to save more and invest strategically in Vanguard Retirement Long-Term Funds (Target Outcome), helping more Americans and their families to save more for their retirement (Desired Impact).

With both our concepts, we have decided to focus on long-term solutions i.e solving at the generational-level.

With both our concepts, we have decided to focus on long-term solutions i.e solving at the generational-level.

4

The Vanguard Group

What sets them Apart?

-

Value of Ownership

-

Cost-friendly

-

Low Expense Ratios

-

Long-term Investing

-

Great Customer Service

Vanguard’s Core Purpose

To take a stand for all investors, to treat them fairly, and to give them the best chance for investment success.

Vanguard is owned by the funds managed by the company and is therefore owned by its customers.

"They created an institution which was pro-customer"

“Because our investors are our owners, we can consistently pass along economies of scale and lower the cost of investing, so they keep more of their returns.”

5

Primary & Secondary Research

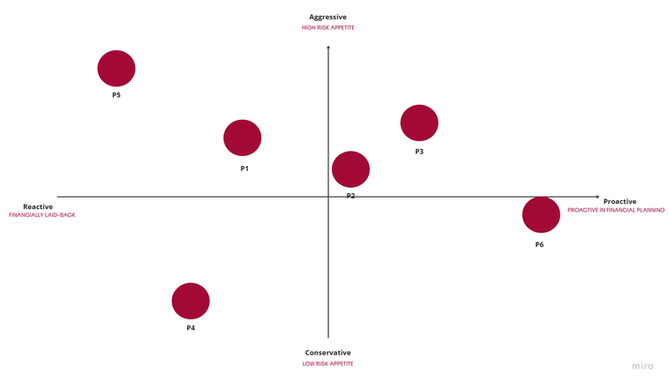

The research phase of our project involved a comprehensive approach to understanding the retirement crisis. Through primary research, including interviews with individuals across different age groups, we gained valuable insights into their financial behaviors and attitudes towards retirement planning. These interviews helped us identify common challenges and informed the development of our user archetypes and opportunity hypotheses.

Additionally, extensive secondary research deepened our understanding of retirement savings trends, financial education, and the role of technology in retirement planning.

By combining insights from both primary and secondary research, we developed a robust foundation for our project, ensuring our strategies and solutions are well-informed and relevant.

Summary

Participant Demographics

-

Age Range: 23 to 55 years old

-

Number of Participants: 6

Common Themes

-

Strong Focus on Retirement

-

Interest in Early Investing

-

Balancing Finances

-

Financial Literacy

-

Customized Financial Tools

Insights

Insights

Early Planning

-

Financial Challenges

-

Education Opportunities.

Parents

-

High Motivation

-

Balancing Goals

Working Professionals

-

Value Stability.

-

Customizable Tools.

Young Investors

-

Risk Tolerance

-

Investment Strategy

Secondary Research

Retirement Funds in the Market

-

Traditional IRA

-

Roth IRA

-

SEP-IRA

-

SIMPLE IRA

-

401(k)

-

Solo 401(k)

-

403(b)

-

Annuity

Players in the Market

-

Vanguard

-

Fidelity

-

T. Rowe Price

-

BlackRock

-

American Funds

-

CreditKarma

-

NerdWallet

-

Empower

Market Share

-

Vanguard, along with other major asset managers like Fidelity, T. Rowe Price, BlackRock and American Funds, collectively controls about 80% of the market share in target-date funds.

-

This significant market share highlights Vanguard's prominent position in the retirement funds sector, especially in managing assets designated for retirement planning through various fund options.

6

User Archetypes

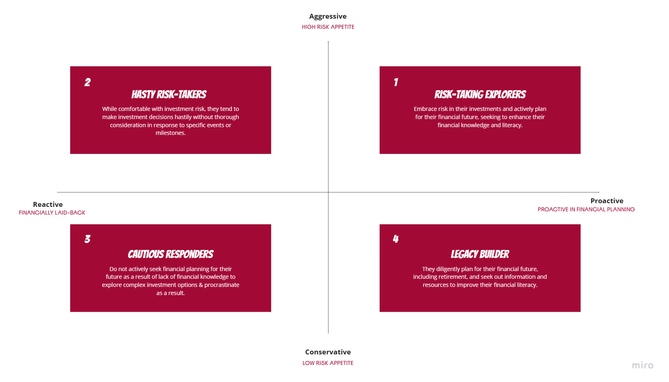

Our project identified four distinct user archetypes based on risk appetite and financial planning behavior.

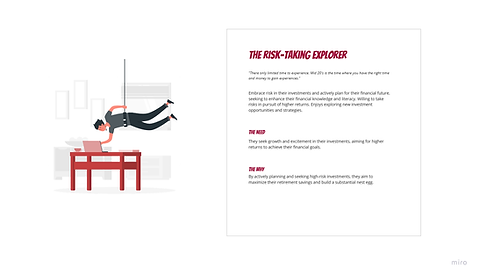

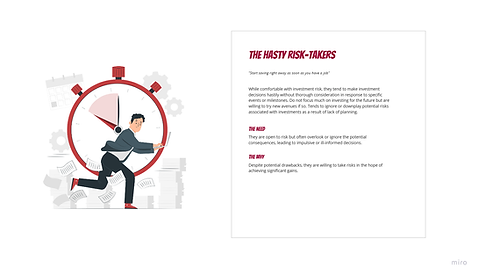

These archetypes include Risk-taking Explorers, who are proactive in financial planning and have a high risk appetite; Hasty Risk Takers, who also have a high risk appetite but take a more laid-back approach to planning; Cautious Responders, who are reactive in financial planning and have a low risk appetite; and Legacy Builders, who are proactive planners with a low risk appetite.

These archetypes allow us to tailor our solutions to meet the needs and behaviors of target user groups.

7

Opportunity Hypothesis 01

OP1

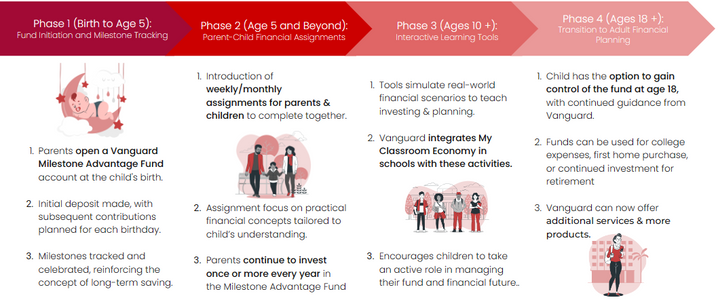

Vanguard Milestone Advantage Fund

01

What is It?

Imagine a future where every milestone in your child's life, such as a birthday is not just a reason for celebration but also a step towards a financially secure tomorrow.

That's what Vanguard's Milestone Advantage Fund looks to achieve

It empowers parents to invest in their child's future with every birthday & significant life event - from day one!

"Vanguard understands the importance of starting early & that's what it looks to convey".

Imagine Vanguard also provides No-Cost financial literacy tools & activities for your children - think basic money management, saving, investing & the importance of long-term planning.

Now, you're not just saving for your child but also inculcating valuable financial skills & good habits early on.

So bottom-line,

A specialized fund that allows all parents to systematically invest in their child’s future from birth, aligning contributions with important milestones like birthdays.

How Does it Work?

-

Setup: Parents open a fund when their child is born.

-

Contributions: Investments made on birthdays and other key milestones/events(at least once a year).

-

Investment Growth: Funds grow over time with the market.

Benefits

-

Ease: Set up once and the fund manages the rest.

-

Connection: Each investment marks a special moment, enhancing the emotional value of saving.

-

Inclusivity: Accesible to all families

-

Security: Builds a financial safety net for the child’s future needs, like education or a first home.

02

Where To Play?

-

What is the opportunity space?

-

Who are you designing for and what is important to them?

-

What are the goals and anticipated outcomes?

-

What is the market context?

Target Archetypes

The Cautious Responder

The Legacy Builder

Market Context

Existing investment options for children are often complex and lack the emotional connection that milestones like birthdays provide. Parents are increasingly seeking ways to secure their child's financial future early on.

Opportunity Space

There is a gap in the market for a financial product that combines the emotional significance of milestones like birthdays with long-term financial planning.

Goals & Anticipated Outcomes

-

Motivate parents to save early and invest wisely.

-

Provide a simple and engaging way for parents to invest in their child's future.

-

instilling a habit of financial planning from a young age.

-

Providing early financial literacy education to children in the form of regular exercises (think, Kumon) - free of cost irrespective of having the fund with Vanguard.

Target Audience

Parents/To-Be Parents

Children

Immigrant Families

Where To Play?

The "Where to Play" for Opportunity Hypothesis 01 revolves around tapping into the emotional significance of milestones like birthdays for new parents or parents-to-be. The goal is to provide a simple and emotionally rewarding investment option that instills a habit of financial planning from a young age. This opportunity arises from the market context where existing investment options for children lack the emotional connection that milestones provide, and parents are increasingly seeking ways to secure their child's financial future early on.

03

How to Win?

-

Who is using the product / service?

-

What problem(s) does it solve?

-

How does it create value for them and you?

-

How will it work?

-

Where does it impact the user’s journey and/or lifecycle?

1. Personalization

-

Combine retirement savings for child with financial education growth.

-

Personalize milestone deposits - adds a personal touch to do something meaningful on an important day.

-

Convey a story - an emotional aspect to provide for family’s future as a gift.

Investing on Birthdays adds a personal touch

"Getting to do something on an important day"

Vanguard conveys a story. An authentic story that conforms to the worldview of a parent looking to save for their child's financial future.

Highlight emotional aspects - providing for family's future - A gift from parent to child

2. Outreach

-

Influencer and Social Media Engagement & Outreach

-

Word-of-Mouth

3. No-Cost Financial Education

-

No cost financial education to everyone, no questions asked.

-

Acts as a “Free-Prize Inside”.

-

Acts as an after-school Financial Literacy program (similar to Kumon)

-

Long-term benefit of teaching a child valuable financial skills.

The “Free Prize Inside” concept aims at offering more than what a customer is paying for (think free Tazos in a bag of Cheetos).

In this case, the free Financial activities for children - no questions asked!

04

User Journey Map

05

Business Model Canvas

06

Market Size

1. Total Addressable Market (TAM)

-

Target Group: Parents of Children aged 0-10 in the U.S.

-

Total Children: 40 million

-

Avg. 1.75 children per family

-

-

Estimated ~23M families

-

Assumption: Every family contributes $4,000 annually.

-

Calculation: TAM = 23 million families × $4,000 each = $92 billion (AUM)

2. Serviceable Addressable Market (SAM)

-

Capture Rate: 50% of the families are assumed to be interested in financial planning products tailored for children’s futures.

-

Contributing Families: 23 million × 50% = 11.5 million families

-

Assumption: Each family contributes $4,000 annually.

-

Calculations:

-

SAM: 11.5 million families x 4000 each = $46 billion (AUM)

3. Serviceable Obtainable Market (SOM)

-

Realistic Market Capture Rate: 30% of contributing families in the initial years.

-

SOM: 11.5M x 30% conversion rate = 3.5 million families

-

SOM value: 3.5 million families × $4,000 per family = $13.8 billion AUM

Key Points

Significant Opportunities: Expanding the target age range to 0-10 years substantially increases the potential market size and the economic impact of the fund.

-Early Engagement: This broader focus allows the fund to capture contributions for a longer period per child, enhancing the potential growth through compounding and establishing a more extended customer relationship.

07

Roadmap

8

Opportunity Hypothesis 02

OP2 Vanguard Spark

01

This innovative mobile platform is designed to help you save for a secure retirement in a fun and engaging way. It combines the power of artificial intelligence (AI) and gamification to personalize your experience and motivate you to reach your financial goals

.png)

What is It?

Benefits

-

Save More & Earn More & Grow More

-

Learn & Make Smart Choices

-

Stay Motivated & Engaged

-

Unlock Rewards & Perks

02

Where To Play?

-

What is the opportunity space?

-

Who are you designing for and what is important to them?

-

What are the goals and anticipated outcomes?

-

What is the market context?

Target Archetypes

The Risk-Taking Explorer

The Legacy Builder

Market Context

There is a growing interest & awareness in financial planning and investing among younger generations and a need for personalized and engaging financial tools that cater to different risk appetites and financial goals.

Opportunity Space

-

Engaging users through gamification, rewards and behavioral science.

-

Providing a behavior-powered rewards platform.

-

Enhanced for those who are proactive in financial planning.

-

Encourage smart investing & savings habits.

Goals & Anticipated Outcomes

-

Motivate users to save more and invest wisely.

-

Rewarding individuals for good financial behaviors & habits.

-

Offering better interest rates and other incentives on their retirement plan.

-

Improving personal finance literacy via experiential learning is built into the process.

Target Audience

Students

Early-Career Professionals

Where To Play?

The opportunity lies in providing a behavior-powered rewards platform that caters to the needs of Risk-Taking Explorers and Legacy Builders, who are proactive in financial planning. This platform should offer gamified features and incentives to encourage smart investing and savings habits. Risk-Taking Explorers and Legacy Builders are the primary targets. They value growth, long-term financial security, and are open to innovative financial solutions.

03

How to Win?

-

Who is using the product / service?

-

What problem(s) does it solve?

-

How does it create value for them and you?

-

How will it work?

-

Where does it impact the user’s journey and/or lifecycle?

-

AI-powered Engagement with Gamification and Interest Rate Boosts

-

Employer Matching Contributions and Milestone-Based Rewards

-

Retirement Impact Visualization

-

Community Building and Peer-to-Peer Learning

-

AI-powered Engagement with Gamification and Interest Rate Boosts

-

Employer Matching Contributions and Milestone-Based Rewards

-

Retirement Impact Visualization

-

Community Building and Peer-to-Peer Learning

04

User Journey Map

05

Business Model Canvas

06

Market Size

1. Total Addressable Market (TAM)

-

U.S. Population (2023): 338.1 million

-

Working-Age (18-67): 63.1%

-

Working-Age Population: 214.3 million

-

Average Contribution: $5,000

-

TAM: $1.071 Trillion (AUM)

2. Serviceable Addressable Market (SAM)

-

Target Age Group: 18-45 years old

-

Estimated Population: 120 million

-

Likelihood to Save for Retirement: 40%

-

Average Contribution: $5,000

-

SAM: $240 Billion (AUM)

07

Roadmap

“

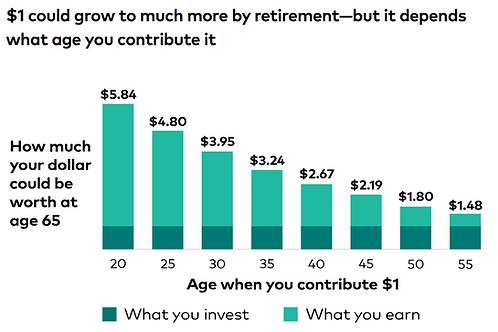

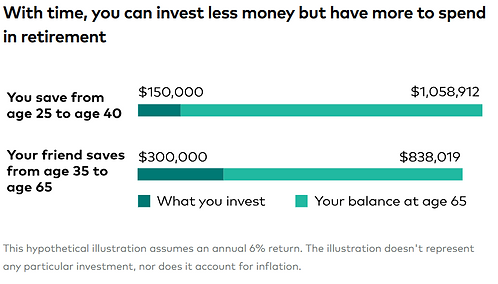

Enjoy the magic of compounding returns. Even modest investments made in one's early 20s are likely to grow to staggering amounts over the course of an investment lifetime.

John C. Bogle, Founder of Vanguard

9

The Magic of Compounding

Concluding Remarks

Making customers - especially younger audience - realize the power of compounding can greatly benefit Vanguard’s pitch on long-term investments.

We believe Vanguard should (in the larger strategic picture) convey a narrative of the importance of compounding & the need to start investing early.

Beginning to save in one’s 20s can be advantageous,

“Imagine it starts at day ONE”

References

-

Image Courtesy: Freepik https://www.freepik.com

-

My Classroom Economy: https://www.vanguardjobs.com/career-blog/2023/03/30/myce-finanicial-literacy/

-

CNBC: Jack Bogle https://www.cnbc.com/2023/11/10/t-bill-and-chill-why-jack-bogles-strategy-of-lazy-investing-is-making-a-comeback-.html